Most board committees operate in quarterly cycles that barely connect to their actual charter mandates. You get an audit committee that meets four times a year because that's what everyone does, not because their charter requires specific deliverables at specific intervals. The compensation committee reviews executive packages in February because that's when they've always done it, not because there's a strategic reason tied to performance cycles or market data availability.

The disconnect creates real governance gaps. Charter language gives committees broad authority — "oversee financial reporting integrity" or "ensure appropriate executive compensation" — but no operational framework for turning that authority into structured work. Committees end up reactive, dealing with whatever management brings them rather than proactively executing their oversight responsibilities.

Why committee charters fail as operational documents

Committee charters read like legal documents because that's what they are. Written by lawyers, approved for compliance, filed away. They establish authority boundaries and liability protections but provide zero guidance on actual work execution.

A typical audit committee charter runs 8-12 pages covering independence requirements, NYSE listing standards, rotation policies, and dozens of "the committee shall" statements. Nowhere does it specify that Q1 meetings should focus on year-end audit wrap-up and internal control testing plans, Q2 on reviewing quarterly results and cybersecurity assessments, Q3 on audit planning for the following year, and Q4 on evaluating auditor performance and fee negotiations.

The operational translation never happens. New committee chairs inherit these charters like ancient scrolls — important but impractical. They know they're supposed to "review and assess the adequacy of internal controls" but not whether that means quarterly testing reports, annual assessments, or something else entirely.

This gap becomes visible during regulatory reviews. An SEC investigation into accounting irregularities can reveal that an audit committee met quarterly but never established a systematic review process for revenue recognition policies — a core charter responsibility. The committee technically fulfilled its meeting obligations but failed its substantive oversight mandate.

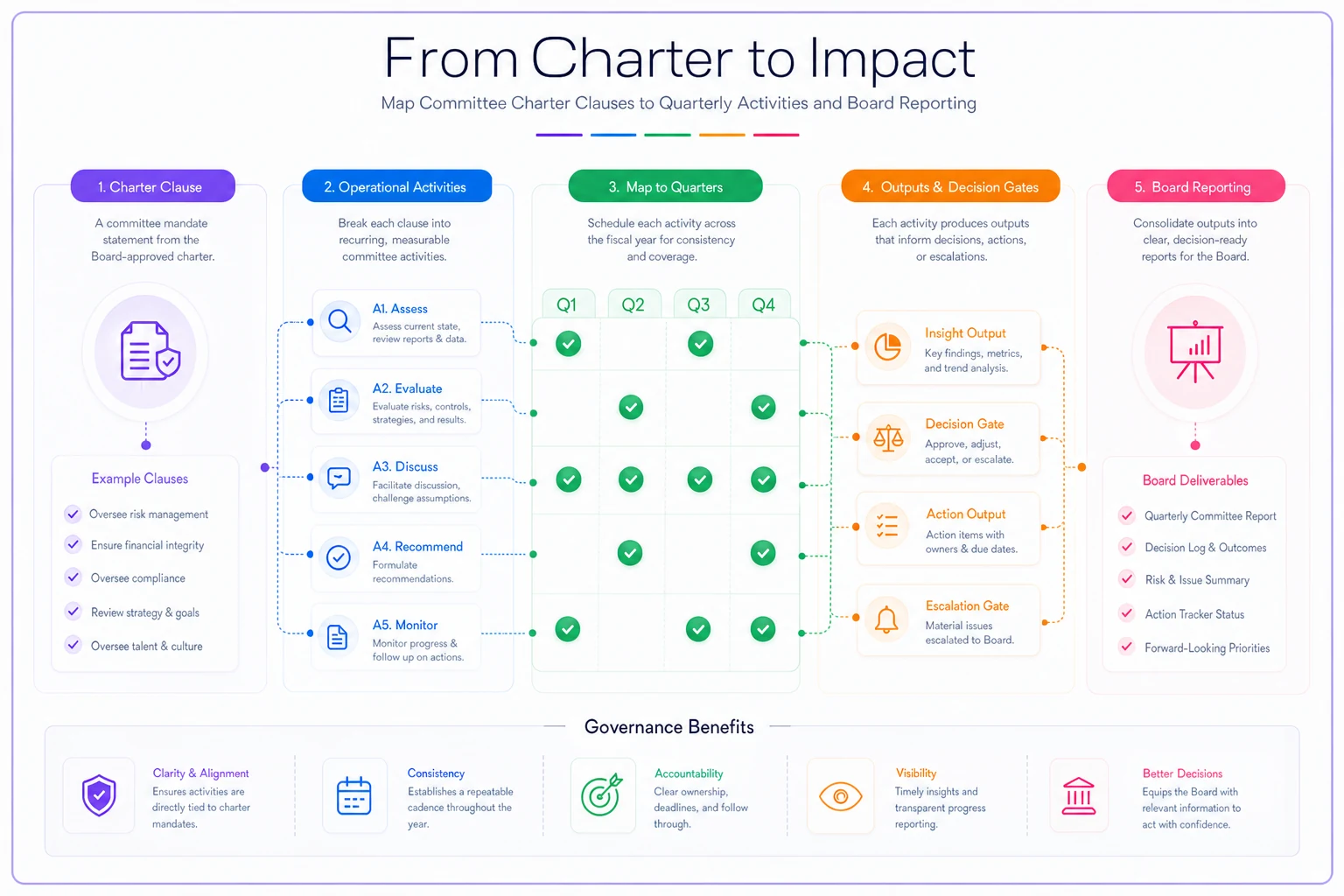

Mapping charter clauses to quarterly deliverables

The solution is treating charter language like requirement specifications that need operational decomposition. Each broad mandate breaks down into specific activities, each activity maps to a quarterly schedule, and each scheduled item produces defined deliverables.

Eliminate boardroom chaos with seamless coordination.

Panlly simplifies scheduling, collaboration, and follow-ups for every board meeting.

- Centralized meeting scheduling

- Secure document sharing

- Task assignment & tracking

No credit card required

Take the standard audit committee responsibility: "Review the company's financial reporting process and disclosure controls."

-

Q1

Review prior year 10-K drafts, management representation letters, and control deficiency remediation status

-

Q2

Assess Q1 earnings quality metrics, review disclosure committee output, evaluate press release consistency

-

Q3

Deep dive on critical accounting estimates, review policy changes for upcoming reporting

-

Q4

Pre-approve audit fees and scope, review internal audit's annual risk assessment

Here's a simple workflow illustrating mapping charter clauses to quarterly deliverables.

The mapping forces specificity. Instead of a vague "review financial reporting," the committee knows exactly what to review, when, and what output to produce.

Audit Committee workplan template

Quarter 1 Focus: Year-end reporting and control environment reset

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Oversee external audit | Review audit findings and management letter | Formal response to auditor recommendations | Approve remediation timeline |

| Monitor internal controls | Assess prior year deficiencies and testing results | Control improvement roadmap | Sign off on testing scope for current year |

| Review financial statements | Deep review of 10-K including MD&A and footnotes | Commentary letter to management | Recommend full board approval |

| Oversee internal audit | Review annual audit plan and resource requirements | Approved audit calendar | Authorize budget and headcount |

Key Q1 Questions:

-

Did any audit adjustments indicate systematic issues?

-

Are control deficiencies concentrated in specific areas?

-

Does internal audit have sufficient resources for the approved plan?

Quarter 2 Focus: Quarterly reporting and emerging risks

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Monitor quarterly results | Review Q1 10-Q and earnings materials | Quality of earnings assessment | Approve for filing |

| Assess disclosure controls | Evaluate disclosure committee effectiveness | Process improvement recommendations | Mandate changes if needed |

| Review whistleblower process | Analyze Q1 hotline reports and investigations | Trend analysis report | Escalate patterns to full board |

| Monitor cyber risks | Review security assessment and incident reports | Risk mitigation priorities | Approve investment requirements |

Key Q2 Questions:

-

Are quarterly results consistent with audit committee expectations?

-

Do whistleblower reports indicate cultural or control issues?

-

Is cyber risk management keeping pace with threat evolution?

Quarter 3 Focus: Forward planning and policy updates

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Review accounting policies | Assess upcoming standards and implementation | Policy change timeline | Approve implementation approach |

| Evaluate audit quality | Mid-year auditor performance review | Performance scorecard | Determine if RFP needed |

| Oversee risk management | Review enterprise risk assessment update | Heat map with mitigation status | Prioritize risk investments |

| Monitor regulatory compliance | Review regulatory correspondence and inquiries | Compliance status dashboard | Approve response strategies |

Key Q3 Questions:

-

Will accounting changes require system updates or training?

-

Is auditor performance meeting committee expectations?

-

Are new regulations creating compliance gaps?

Quarter 4 Focus: Annual assessments and next year preparation

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Approve audit fees | Review fee proposal and scope changes | Fee recommendation | Approve for shareholder proxy |

| Assess committee performance | Conduct self-evaluation against charter | Performance report with gaps | Approve charter amendments |

| Review related party transactions | Annual review of all related party deals | Independence assessment | Approve or require modifications |

| Evaluate internal audit | Annual performance and independence review | Effectiveness report | Approve compensation changes |

The template creates accountability. Each quarter has specific outputs tied directly to charter language. Missing a deliverable means failing a charter requirement — that connection makes the work concrete rather than abstract.

Finance Committee workplan template

Finance committees often overlap with audit committees in smaller organizations, but their distinct focus on capital allocation, treasury, and strategic finance requires different quarterly rhythms.

Quarter 1 Focus: Capital planning and prior year assessment

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Oversee capital structure | Review debt capacity and credit facility usage | Refinancing recommendations | Approve debt strategy |

| Monitor cash management | Assess cash flow forecasts and working capital | Liquidity risk assessment | Set minimum cash thresholds |

| Review investment policy | Evaluate portfolio performance and compliance | Investment policy updates | Approve manager changes |

| Guide dividend policy | Analyze payout ratios and peer benchmarks | Dividend recommendation | Propose to full board |

Quarter 2 Focus: Mid-year adjustments and investment reviews

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Approve major investments | Review capital project proposals over threshold | ROI analysis and recommendations | Approve or reject projects |

| Monitor banking relationships | Assess bank service quality and fees | Relationship scorecard | Authorize RFPs if needed |

| Review insurance coverage | Evaluate coverage adequacy and pricing | Insurance program changes | Approve coverage modifications |

| Oversee pension funding | Review funded status and assumption changes | Contribution recommendations | Approve funding levels |

Quarter 3 Focus: Strategic finance and market assessment

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Evaluate M&A opportunities | Review pipeline and valuation models | Priority target list | Authorize due diligence |

| Monitor investor relations | Assess shareholder feedback and concerns | IR strategy adjustments | Approve messaging changes |

| Review hedging strategies | Evaluate FX and commodity exposures | Hedging policy updates | Approve hedge execution |

| Guide financial planning | Review long-range plan assumptions | Scenario analysis | Endorse planning framework |

Quarter 4 Focus: Budget approval and next year setup

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Approve annual budget | Deep dive on revenue and expense assumptions | Budget recommendation | Submit to full board |

| Set performance metrics | Define financial targets and thresholds | KPI dashboard | Lock incentive targets |

| Review tax strategy | Assess tax planning opportunities and risks | Tax provision adjustments | Approve strategies |

| Evaluate finance function | Review department capabilities and needs | Organization recommendations | Approve headcount changes |

Quarter 4 Focus: Budget approval and next year setup

Compensation Committee workplan template

Compensation committees face unique timing pressures — proxy deadlines, performance periods, market data availability. Their workplan has to synchronize with these external constraints while still maintaining systematic oversight.

Quarter 1 Focus: Prior year finalization and proxy preparation

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Determine executive compensation | Calculate final bonus payouts and equity vesting | Compensation decisions | Approve payments |

| Oversee proxy disclosure | Review CD&A and compensation tables | Proxy compensation section | Approve for filing |

| Assess pay-for-performance | Analyze TSR and peer comparisons | Pay alignment analysis | Adjust if misaligned |

| Review severance agreements | Update change-in-control provisions | Agreement modifications | Approve new terms |

This committee's work intensifies around proxy season. They can't spread decisions evenly across quarters — February decisions drive March proxy filings which determine April shareholder votes.

Quarter 2 Focus: Shareholder feedback and plan design

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Monitor shareholder views | Review say-on-pay results and feedback | Response strategy | Implement changes |

| Design incentive plans | Develop next year's STIP/LTIP framework | Plan design document | Approve structure |

| Review equity usage | Assess burn rate and overhang levels | Equity management strategy | Adjust grant guidelines |

| Evaluate compensation consultant | Review advisor independence and effectiveness | Consultant assessment | Renew or replace |

Quarter 3 Focus: Market assessment and competitive positioning

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Benchmark compensation | Review peer group and market data | Competitive assessment | Approve peer changes |

| Assess retention risk | Identify key talent and flight risks | Retention strategies | Approve special awards |

| Review clawback policy | Ensure compliance with Dodd-Frank | Policy updates | Approve modifications |

| Monitor diversity metrics | Assess pay equity and representation | DEI compensation analysis | Address gaps |

Quarter 4 Focus: Target setting and forward planning

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Set performance goals | Establish next year's financial/operational targets | Goal recommendation | Lock targets |

| Approve base salaries | Review market adjustments and merit increases | Salary decisions | Approve increases |

| Grant equity awards | Determine grant sizes and types | Award recommendations | Approve grants |

| Review succession planning | Assess bench strength and development needs | Succession readiness report | Identify gaps |

Quarter 4 Focus: Target setting and forward planning

Nominations and Governance Committee workplan template

The Nominations Committee drives board composition and governance practices — work that seems episodic but requires constant cultivation.

Quarter 1 Focus: Board assessment and planning

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Evaluate board performance | Conduct annual board/committee assessments | Assessment report | Share with full board |

| Review board composition | Analyze skills matrix and diversity metrics | Gap analysis | Initiate searches |

| Oversee director education | Plan education sessions and conferences | Education calendar | Approve budget |

| Update governance policies | Review policy changes and best practices | Policy updates | Approve changes |

Unlike other committees that respond to business cycles, Nominations has to think in board terms — three-year director terms, age limits, refreshment targets. Their quarterly work builds toward annual director slates.

Quarter 2 Focus: Director recruitment and AGM preparation

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Identify director candidates | Review search firm recommendations | Candidate slate | Approve interviews |

| Prepare proxy governance section | Draft director bios and governance disclosures | Proxy governance section | Submit to full board |

| Review shareholder proposals | Assess governance-related proposals | Response recommendations | Determine positions |

| Monitor governance ratings | Review ISS/Glass Lewis assessments | Rating improvement plan | Implement changes |

Quarter 3 Focus: Onboarding and committee optimization

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Onboard new directors | Execute comprehensive integration plan | Onboarding confirmation | Verify readiness |

| Review committee composition | Assess committee effectiveness and rotation | Composition changes | Approve assignments |

| Update committee charters | Review charter adequacy and compliance | Charter amendments | Approve updates |

| Oversee ethics program | Review code of conduct training and violations | Ethics report | Address issues |

Quarter 4 Focus: Governance evolution and next year setup

| Charter Requirement | Operational Activity | Deliverable | Decision Gate |

|---|---|---|---|

| Plan board calendar | Set meeting dates and agenda priorities | Annual calendar | Full board approval |

| Review D&O insurance | Assess coverage and litigation trends | Insurance recommendations | Approve renewal |

| Evaluate governance structure | Consider board/committee size and structure | Structure recommendations | Propose changes |

| Assess ESG oversight | Review ESG governance and reporting | ESG governance framework | Assign oversight |

Quarter 4 Focus: Governance evolution and next year setup

Building decision gates that matter

Decision gates transform committee meetings from discussion forums into actual decision-making sessions. Each gate represents a point where the committee must commit — approve, reject, or escalate. Without them, committees can talk about topics endlessly without landing anywhere.

Effective gates share three characteristics:

Binary clarity: The decision is yes/no, not "let's revisit next quarter." If management presents the annual audit plan, the committee either approves it or sends it back for revision. No middle ground.

Documented rationale: The decision includes why, not just what. Approving a $2M increase in audit fees requires documenting the scope changes, complexity factors, or regulatory requirements driving the increase.

Downstream triggers: Each decision activates something — a process, a communication, a timeline. Approving the compensation consultant's recommendations triggers proxy disclosure drafting, shareholder outreach planning, and grant agreement preparation.

Creating feedback loops to the full board

Committee work means nothing if it doesn't inform full board decisions. Yet many boards treat committee reports as FYI updates rather than decision inputs. The audit committee chair presents for five minutes, directors nod, everyone moves on.

Structured feedback loops change this. Each committee workplan should identify specific touchpoints where committee work requires full board engagement:

Pre-decision consultations: Before the compensation committee finalizes CEO compensation, they present the framework to the full board for input. Not approval — input. This prevents surprise objections during final approval.

Risk escalation triggers: The audit committee defines specific thresholds that automatically elevate issues to the full board. A material weakness in internal controls, a disagreement with external auditors, or cybersecurity incidents above defined severity levels trigger immediate board notification.

Integrated planning cycles: Committee workplans synchronize with full board planning. The finance committee's capital allocation review in Q2 feeds the board's strategy session in Q3. The nominations committee's board assessment in Q1 drives the board's governance workshop in Q2.

Cross-committee coordination: Modern governance issues rarely fit neatly in one committee. ESG touches audit (reporting), compensation (incentives), and nominations (board expertise). Workplans need to identify these overlaps and create joint sessions or sequential reviews that prevent gaps or redundancies.

The operational reality of committee coordination

The templates above look clean on paper, but actual operations are messier. A cyber incident in Q2 disrupts the audit committee's planned agenda. An activist investor in Q3 forces the governance committee to accelerate director searches. A CFO departure in Q4 scrambles the finance committee's entire budget approval process.

This is where AI-powered operational software starts to matter. Static Word documents become obsolete after the first crisis. What committees actually need are dynamic workplans that adapt while still maintaining compliance with charter requirements.

Use a centralized action-tracking system to avoid lost follow-ups and enforce accountability on decision gates.

Think about tracking dozens of charter requirements across four committees, each with quarterly deliverables, decision gates, and board reporting obligations. Doing that manually through spreadsheets and email chains guarantees things get dropped. Critical decisions get delayed because someone forgot to send the pre-read. Follow-up items disappear entirely because there's no systematic tracking in place.

Modern board management platforms address this through intelligent automation. They can parse charter language to identify requirements, map those requirements to quarterly calendars, and track completion status in real time. When the audit committee approves the internal audit plan in Q1, the system automatically schedules quarterly progress reviews and flags delayed audits before they become a problem.

These platforms also preserve institutional knowledge in a way manual systems can't. New committee chairs inherit not just a charter but a complete operational history — what decisions were made, why, what worked, what didn't. That context alone prevents committees from rehashing old debates or quietly dropping established practices that nobody remembered existed.

Measuring committee effectiveness through workplan execution

The real test of these workplans isn't how comprehensive they look — it's execution rate. A committee that completes 90-95% of planned deliverables demonstrates operational discipline. One that constantly defers items or produces shallow outputs is signaling a deeper problem.

Tracking execution patterns reveals a lot:

-

Which charter requirements consistently get shortchanged?

-

Which quarters have the most deferrals?

-

Which deliverables consistently take longer than planned?

-

Which decision gates create bottlenecks?

These patterns drive workplan refinement. Maybe Q4 is too ambitious given year-end pressures. Maybe certain charter requirements only need bi-annual review rather than quarterly. The workplan evolves from static template into something that actually reflects how the committee operates.

Beyond compliance to strategic value

The best committee workplans go beyond compliance checkboxes. The audit committee doesn't just review financial statements — they challenge management's assumptions and push for better disclosure. The compensation committee doesn't just approve pay packages — they design incentives that actually drive long-term value creation.

That elevation happens when committees shift from reactive to proactive. Instead of responding to whatever management brings them, they request specific analyses. Instead of accepting standard reports, they ask for custom metrics. Instead of reviewing historical results, they push toward leading indicators.

The workplan templates support this shift when used intentionally. The Q3 audit committee review of critical accounting estimates is timed to influence Q4 budget assumptions. The Q2 compensation committee market analysis positions the company for Q3 talent decisions. The Q1 nominations committee board assessment drives Q2 director recruitment priorities.

Committee effectiveness ultimately depends on translating broad charter mandates into specific, scheduled, measurable work. These templates provide the framework, but execution requires discipline, the right tools, and a willingness to refine. The boards that get this right stop treating committees as necessary overhead and start using them as genuine governance infrastructure.

Committee effectiveness ultimately depends on translating broad charter mandates into specific, scheduled, measurable work. These templates provide the framework, but execution requires discipline, the right tools, and a willingness to refine. The boards that get this right stop treating committees as necessary overhead and start using them as genuine governance infrastructure.

Ready to enhance your board's productivity?

Join 500+ organizations using Panlly to save time, improve governance, and streamline board operations.